Target Date 2030

Blackrock lifepath target date 2030 S GBP ACC.

Designed for people retiring around 2030.

Pension

We’ll help you track down and bring your old pensions together under one roof.

It only takes 2 minutes to start the search. And once they're all together you can top up your pension whenever you like.

The value of your pension could go up or down and you could get back less than you put in. You need a free Monzo current account to open a Monzo Pension. 18-70 years old only. UK residents only. Ts&Cs apply.

The App Store, Google Play Store and Trustpilot ratings are correct as of 27 Apr, 2026.

Step 1

Find your old pensions

Tell us where you worked and when - that’s all we need to get started.

Step 2

Consolidate them into one

You’ll see all your old pensions as one, giving you a clear picture of your future.

Step 3

Add money anytime

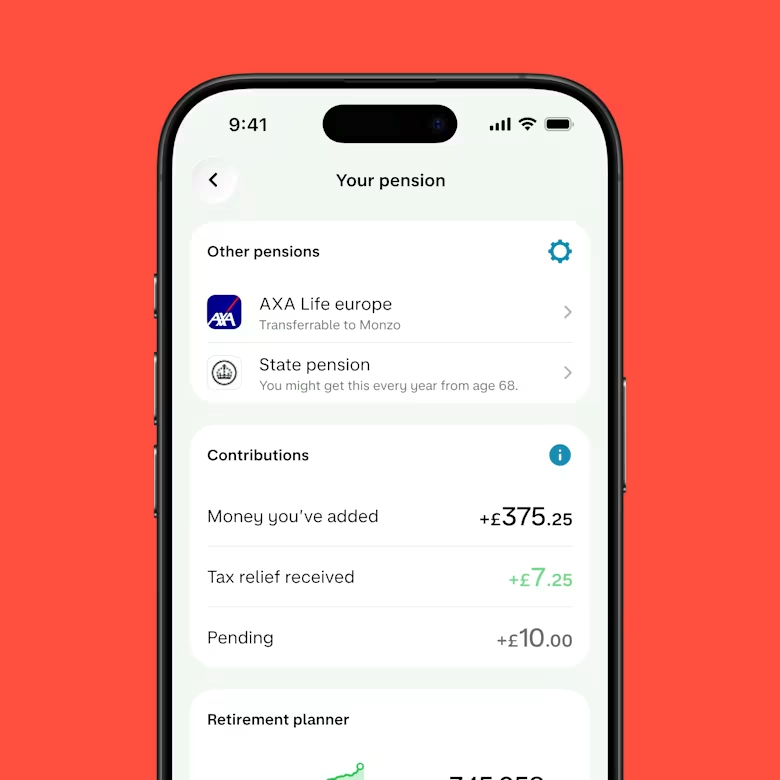

Whether it’s a little or a lot, every bit helps. Plus, you get tax relief whenever you make a pension contribution - that's when the government tops you up. The taxes you pay depend on your circumstances and rules could change in the future.

Share a few details and we’ll predict how much your pension could be worth when you retire.

This prediction isn’t a guarantee of how your pension will grow. It’s an estimate based on assumptions and your details.

Saving for later doesn’t have to be hard work. Finding your pensions and keeping everything in one place means you can stay on top of your retirement goals.

The taxes you pay depend on your circumstances and rules could change in the future. An investment’s past performance doesn’t show how it’ll perform in the future.

Our bite-sized lessons break down pensions for you. Each one is only around 90 seconds, but packed full of key info to help you understand more about your future money. Find them in the app.

Here's what happens behind the scenes.

The average old pension is worth £9,470, and we're the only bank (with some help from our partner Raindrop) that can find yours.

Once they're found, you can bring them together in one place so that they're easier to keep track of.

A Monzo Pension is a self-invested personal pension (SIPP). You can choose how your pension is invested from a range of funds, including target date funds, ready-made funds and geographic funds.

The funds your pension invests in are managed by BlackRock, one of the world’s largest fund managers. They manage the savings of over 13 million UK pension customers.

For your SIPP (Self-Invested Personal Pension), eligible investments are protected by the FSCS up to £85,000 per person, per authorised firm. This protection does not cover losses from investment performance.

You’ll pay a 0.25% yearly platform fee (or 0.20% with Monzo Perks or Max) on your combined investments and pension balance up to £100,000, plus ongoing management fees that depend on what you invest in.

That means your maximum yearly platform fee is capped at £250 (or £200 with Monzo Perks or Max).

Pick a target date fund that automatically adjusts risk as you get closer to retirement, a ready-made fund based on the level of risk you’re comfortable with, or geographic funds focused on certain parts of the world.

Blackrock lifepath target date 2030 S GBP ACC.

Designed for people retiring around 2030.

Blackrock lifepath target date 2035 S GBP ACC.

Designed for people retiring around 2035.

Blackrock lifepath target date 2040 S GBP ACC.

Designed for people retiring around 2040.

Blackrock lifepath target date 2045 S GBP ACC.

Designed for people retiring around 2045.

Blackrock lifepath target date 2050 S GBP ACC.

Designed for people retiring around 2050.

Blackrock lifepath target date 2055 S GBP ACC.

Designed for people retiring around 2055.

Blackrock lifepath target date 2060 S GBP ACC.

Designed for people retiring around 2060.

Blackrock lifepath target date 2065 S GBP ACC.

Designed for people retiring around 2065.

Blackrock lifepath target date 2030 S GBP ACC.

Designed for people retiring around 2030.

Blackrock lifepath target date 2035 S GBP ACC.

Designed for people retiring around 2035.

Blackrock lifepath target date 2040 S GBP ACC.

Designed for people retiring around 2040.

Blackrock lifepath target date 2045 S GBP ACC.

Designed for people retiring around 2045.

Blackrock lifepath target date 2050 S GBP ACC.

Designed for people retiring around 2050.

Blackrock lifepath target date 2055 S GBP ACC.

Designed for people retiring around 2055.

Blackrock lifepath target date 2060 S GBP ACC.

Designed for people retiring around 2060.

Blackrock lifepath target date 2065 S GBP ACC.

Designed for people retiring around 2065.

BlackRock MyMap 3 Select ESG

You’re happy with potentially smaller returns for less risk. About 80% of money in this fund ends up in bonds, and about 20% in shares.

BlackRock MyMap 5 Select ESG

You're aiming for a higher return than Careful, with a medium level of risk. Roughly 34% of money in here ends up in bonds, and about 66% in shares.

BlackRock MyMap 8 Select ESG

You’re happy taking more risk if it means your returns could be higher. 100% of money in this fund ends up in shares.

iShares S&P 500 UCITS ETF

Invest in the biggest businesses listed on US stock exchanges and put your money into companies like Walmart, Netflix and Coca-Cola.

iShares Core FTSE 100 UCITS ETF Accumulating GBP

Invests in the 100 largest companies on the London Stock Exchange. Think big businesses traded on the LSE like Tesco, Vodafone and Unilever.

iShares Core MSCI Europe UCITS ETF Accumulating EUR

Invests across many companies which are traded on European stock exchanges, including companies in industries like fashion, food and tech. Think big companies like Spotify, Nestle and Hermes.

iShares Core MSCI World UCITS ETF

Invests in the world's biggest companies across 23 countries, global stock markets and all sorts of industries. From Apple to Zurich Insurance, this is a good choice if you want a diverse range of investments.

iShares MSCI EM UCITS ETF Accumulating GBP

Emerging markets means countries like China, Brazil, India and South Korea. You'll be tapping into exciting markets and investing in growing businesses across industries like finance, tech and energy.

To get started with a Monzo Pension, all you need is our free Monzo current account, which is packed with helpful ways to manage your money.

Apply in minutes.

Read our guides to help your future money go further.

Sometimes the best things in life are found in PDF links. Check out these important documents about the Monzo Pension.

A Monzo Pension is a type of pension called a SIPP (self-invested personal pension). It gives you the ability to save for your retirement and the freedom to choose how your pension is invested.

A SIPP can be a tax-efficient way to boost your retirement savings. You can have a SIPP alongside other investments, such as the ones inside Stocks and Shares ISAs and workplace pensions. The taxes you pay depend on your circumstances and rules could change in the future.

A SIPP is not designed to replace your workplace pension, if you’re employed, it’s meant to complement and work alongside it.

If you’re self-employed, a SIPP is one way of saving for your retirement.

By combining your pensions into one place, you’ll be able to see exactly how much you’ve built up – and work out if you’re on track for the future.

You usually get a new pension with each new job you have. So it’s easy for pensions to rack up. And over time, this can be difficult to keep track of. You’ll also cut down on future admin as you’ll only need details for one pension when you retire.

And you’ll know exactly what you’re paying for your pensions too. Each provider has their own fees, so it can be tricky to work out what you’re paying when you have several pensions. With a Monzo Pension, you’ll pay transparent fees – you’ll pay a 0.25% platform fee (or 0.20% with Monzo Perks or Max) across your pension and investment accounts up to £100,000, plus ongoing management fees that depend on what you invest in.

That means your maximum annual platform fee is capped at £250 (or £200 with Monzo Perks or Max). Bear in mind, at the point of combining your pension, you may be charged exit fees by your different pension providers, although this is usually capped.

But remember, pension consolidation is a very personal financial decision, and it's not right for everyone. We'd always recommend seeking independent financial advice before combining your pensions.

You can combine old workplace and personal pensions.

You won’t be able to transfer your current workplace pension that you’re paying into. If you’ve already started taking money from a pension, you won’t be able to transfer that. And if your old pension has safeguarded benefits, we won’t transfer that either.

Finding your old pension documents can help us to find and combine your pensions sooner.

It’s best if you know your previous employer’s name, your pension provider’s name, reference number and rough pension value.

But don’t worry if you don’t have all this information. We can still look for your pension – even if all you know is where you worked and when.

You'll pay a 0.25% platform fee (or 0.20% with Monzo Perks or Max) across your pension and investment accounts up to £100,000, plus ongoing management fees that depend on what you invest in.

That means your maximum annual platform fee is capped at £250 (or £200 with Monzo Perks or Max).

Your fees accrue daily, and are charged monthly.

No, not at all. You should continue paying into your current workplace pension as normal.

When you pay into your workplace pension, your employer usually does too (up to a certain amount, which will be agreed in your contract). So you’re likely to get more for your money by contributing to that, rather than a personal pension.

When you pay into your Monzo SIPP, the government gives you a top-up – which is tax relief. For most people, that means for every £80 you put in, the government adds £20, so you end up with £100 in your pension pot.

If you pay a higher rate of tax, you can claim back even more through your tax return, boosting your finances.

Just remember there are limits on how much tax relief you can receive, and it isn't available for everyone. You can read more here.

Yes, absolutely. Monzo Pensions are self-invested personal pensions (SIPPs), which means you decide how much you save and when you contribute, so they’re well suited for anyone who’s self-employed.

Just head to the Pensions area in the app and tap ‘Add money’ to make contributions directly from your Monzo current account whenever you like.

The amount of money you need depends on the lifestyle you want. As a general guide, Retirement Living Standards research suggests a single person roughly needs:

- £14,000 a year for a minimum lifestyle (covering the basics)

- £32,000 a year for a moderate lifestyle (more financial security, holidays)

- £44,000 a year for a comfortable lifestyle (more financial freedom and luxuries).

Use our pension prediction tool to get an idea of the amount you could have when you retire.

You can’t take money out until you turn 55 (rising to age 57 from 6 April 2028), as pensions are legally locked to ensure you have money for retirement. And if you do make an unauthorised early withdrawal, HMRC may charge you up to 55% tax.

The only exceptions for this are if you’re diagnosed with a terminal illness or a condition that means you can never work again.

The government’s Money and Pensions Service can help if you have any questions around pensions or money guidance, and debt advice too.

You should be sure combining your pensions is right for you. Before you make the move, make sure you know your old pension’s fees. If you transfer your pension to one with higher fees, it’ll impact the value of your pension over a long-term period.

And if you’re still unsure, speak to a financial adviser, or if you’re over 50, you can get free and impartial guidance through Pension Wise.